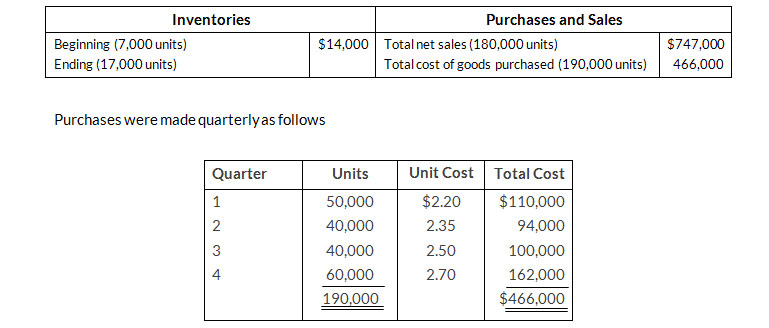

The management of Gresa Inc. is reevaluating the appropriateness of using its present inventory cost flow method, which is average-cost. The company requests your help in determining the results of operations for 2019 if either th FIFO or the LIFO method had been used. For 2019, the accounting records show these data.

Operating expenses were $130,000, and the company's income tax rate is 40%.

Instructions

- Prepare comparative condensed income statements for 2019 under FIFO and LIFO(Show computations of ending inventory)

- Answer the following operations for management.

- Which cost flow method (FIFO or LIFO) produces the more meaningful inventory amount for the balance sheet? Why?

- Which cost flow method (FIFO or LIFO) produces the more meaningful net income? Why?

- Which cost flow method (FIFO or LIFO) is more likely to approximate the actually physical flow of goods? Why?

- How much more cash will be available for management under LIFO than under FIFO? Why?

- Will gross profit under the average-cost method be higher or lower than FIFO? Than LIFO? (Note: It is not necessary to quantify your answer)

Solution

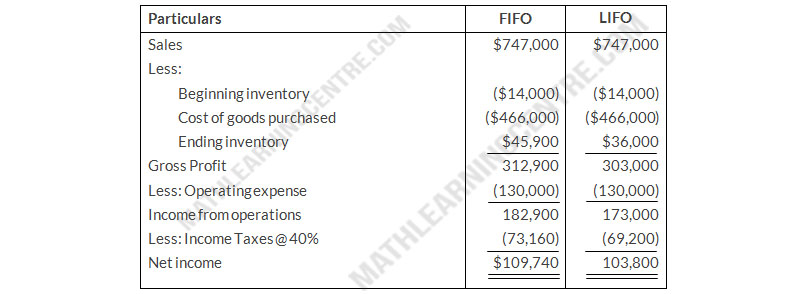

a.

Gresa Inc.

Condensed Income Statement

For the year ended December 31, 2019

Condensed Income Statement

For the year ended December 31, 2019

b.

- FIFO method produces the more meaningful inventory amount for the balance sheet because the units are closed at the most recent purchase

- LIFO method produces the more meaningful net income for the balance sheet because the costs are closed at the most recent purchases against the sales

- FIFO method is more likely to approximate the actual physical flow of goods because the oldest goods are usually sold first to minimize damages and expired

- There will be $3,960 additional cash available for management under LIFO than under FIFO because income taxes are $69,200 under LIFO and $73,160 under FIFO

- Gross profit under the average-cost method will be lower than FIFO and higher than LIFO